*The contents of this blog were updated on March 26, 2026.

Energy storage developers face a complex landscape when deploying new projects, from technical challenges to financial and regulatory hurdles. Understanding where these obstacles arise is critical to designing successful systems and delivering reliable value to customers. Our survey of energy storage developers highlights the current trends, key deployment barriers, and primary factors driving adoption in both residential and commercial markets.

A central theme that emerged is the importance of leveraging an energy management system (EMS) like ETB Controller to optimize performance, model savings accurately, and ensure that battery energy storage systems operate efficiently. By combining technical insights with a clear understanding of project economics, developers can overcome operational challenges and accelerate the deployment of storage projects with confidence.

The Current Focus: Residential, Commercial, or Both

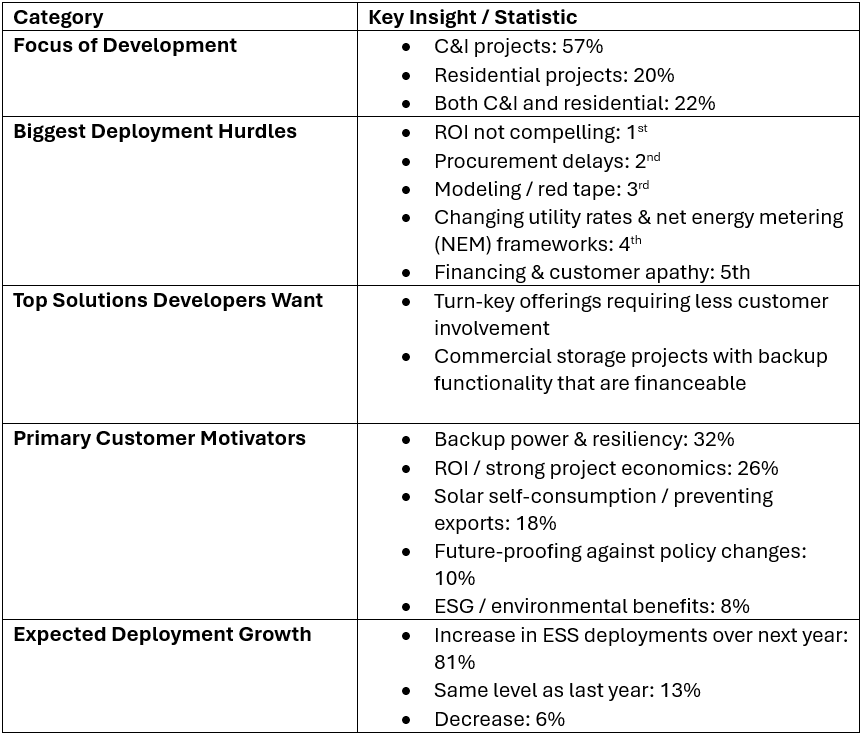

Developers were asked whether they primarily focus on residential or commercial and industrial (C&I) projects. The survey results showed:

- Commercial projects: 57%

- Residential projects: 20%

- Both residential and C&I: 22%

Commercial deployments are clearly leading, reflecting the strong adoption of storage in larger-scale applications where ROI can be more compelling.

Survey Results: Energy Storage Development Trends and Challenges

Key Hurdles in Energy Storage Deployment

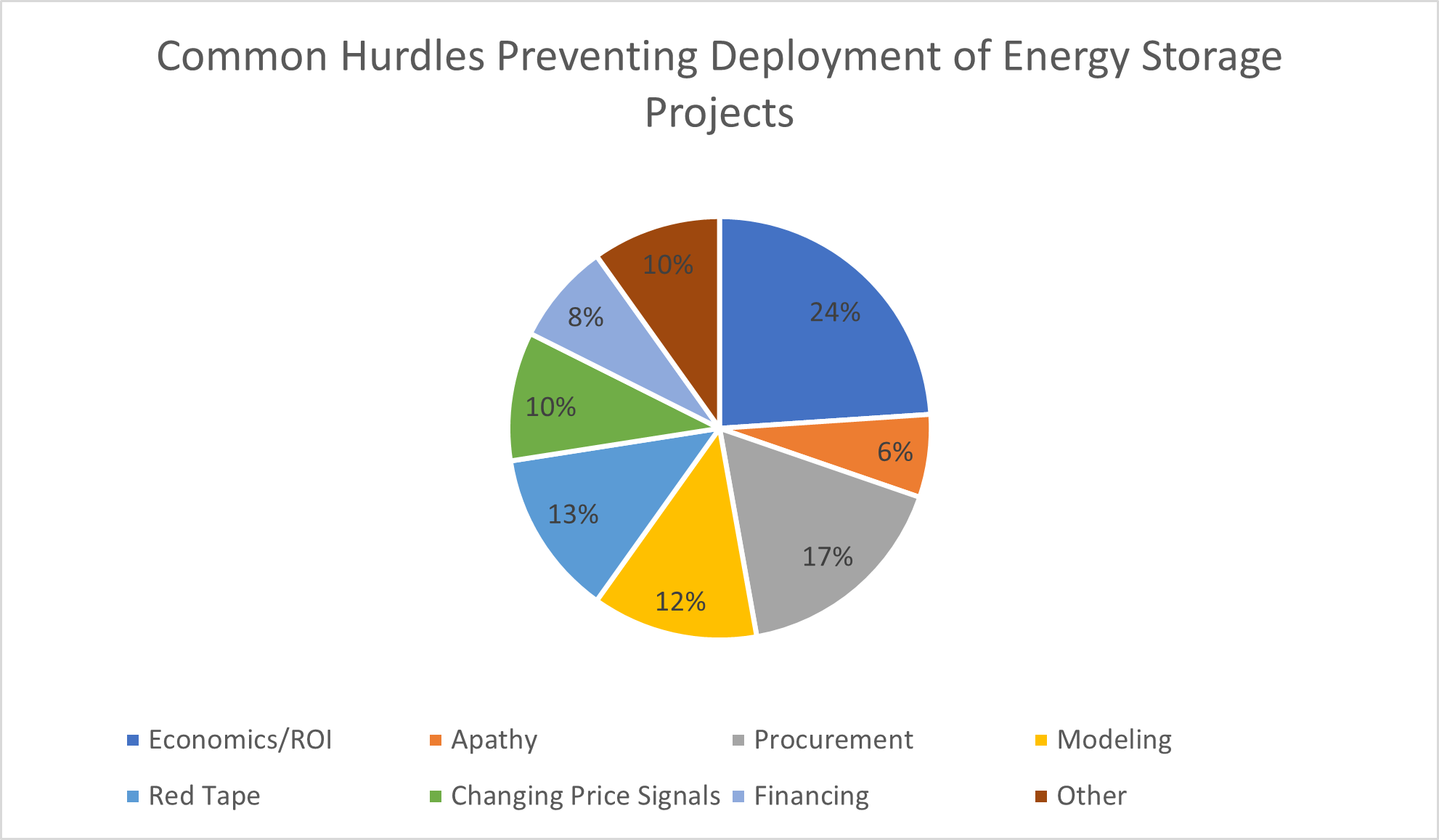

Developers were asked to identify the biggest barriers preventing additional ESS deployments. The top challenges included:

- ROI not compelling enough: Developers cited regional variations in economics; some markets offer strong utility bill savings, while others are less financially attractive. Markets with higher ESS adoption generally correlate with stronger value propositions.

- Procurement challenges: Limited product availability and long lead times create delays, a topic explored in our Battery & Energy Storage System – Supply Chain and Pricing Report.

- Modeling and red tape: Lack of confidence in modeling and presenting ESS savings, coupled with burdensome interconnection processes and permitting or certification requirements, remains a significant hurdle.

- Changing price signals: Utility rates and NEM frameworks fluctuate, complicating financial projections.

- Financing and customer apathy: Limited access to ESS financing or low customer interest, with some customers focused solely on solar, constrains deployments.

Potential Solutions From Developers

When asked what would help them close and deploy more ESS projects, participants highlighted solutions such as:

- “A better turn-key offering that requires less customer involvement”

- “A commercial storage project that fits the cost curve, is financeable, and provides back-up functionality”

These responses underline the importance of simplified deployment workflows and financially viable products with clear operational benefits.

Primary Motivators for Adding Storage

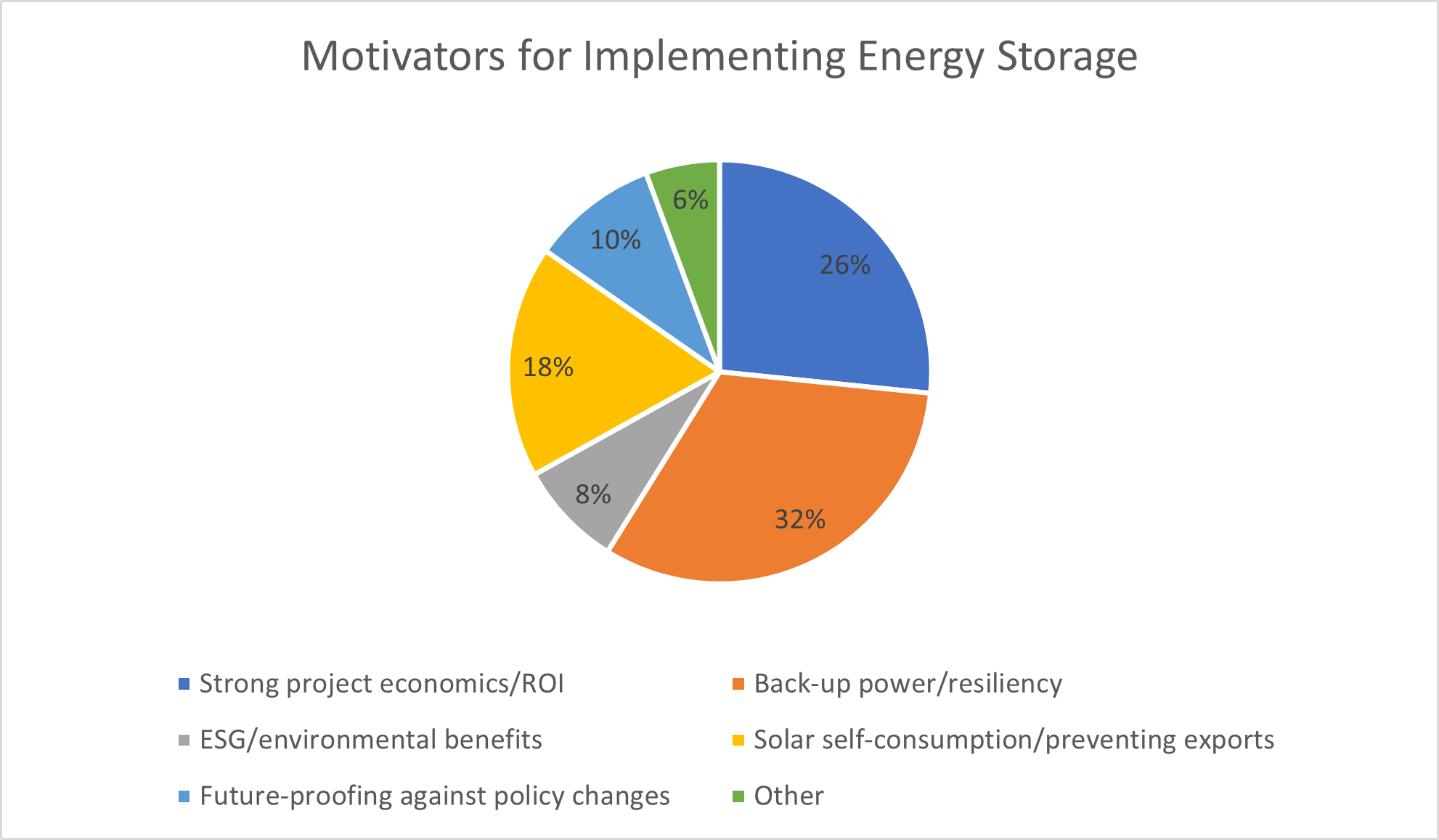

Developers shared the key drivers motivating host customers to add ESS:

- Back-up power and resiliency: 32%

- ROI and strong project economics: 26%

- Solar self-consumption / preventing exports: 18%

- Future-proofing against policy changes: 10%

- ESG and environmental benefits: 8%

Interestingly, back-up power and resiliency lead in overall responses, reflecting strong interest in energy reliability across residential applications. In C&I deployments, ROI remains the primary consideration.

Expectations for Future Sales and Deployments

Developers were asked whether they expect to sell or deploy more ESS projects in the next year compared to the previous year:

- Expect increase: 81%

- Expect the same: 13%

- Expect decrease: 6%

Key Takeaways

The survey highlights several actionable insights for the energy storage market:

- Commercial projects dominate current development activity.

- ROI, procurement delays, and regulatory hurdles remain the most significant barriers.

- Simplified turn-key solutions and financeable storage offerings could accelerate adoption.

- Back-up power, resiliency, and ROI continue to drive customer adoption.

- Most developers expect deployment growth in the year ahead, signaling continued confidence in the market.

By understanding these hurdles and motivators, ESS developers and financiers can better align strategies, streamline workflows, and optimize project economics to accelerate energy storage adoption.