*The contents of this blog were updated on March 26, 2026.

Energy storage deployment is accelerating, yet developers continue to face meaningful obstacles that can delay timelines, increase costs, or undermine project economics. The most significant development hurdles in the energy storage market typically stem from regulatory complexity, evolving incentive structures, financing uncertainty, and challenges within the storage interconnection process. While policy momentum and market demand are strong, successful projects require careful coordination across technical, financial, and operational disciplines, as highlighted in industry analyses such as the Q2 Energy Storage Report.

Understanding where these hurdles arise (and how to proactively address them) can determine whether a project reaches commercial operation on schedule and with expected returns. From tax incentive eligibility and wholesale market participation to interconnection risk and revenue modeling assumptions, developers must approach storage with precision and transparency to reduce uncertainty and protect long-term value.

Federal and State Tax Incentives

Tax incentives remain one of the most important drivers of project economics. However, they are not always straightforward, and legal analysis from firms such as K&L Gates continues to highlight how policy interpretation can impact project eligibility. At the federal level, two mechanisms are central to storage projects:

- Investment Tax Credit (ITC)

- Modified Accelerated Cost Recovery System (MACRS)

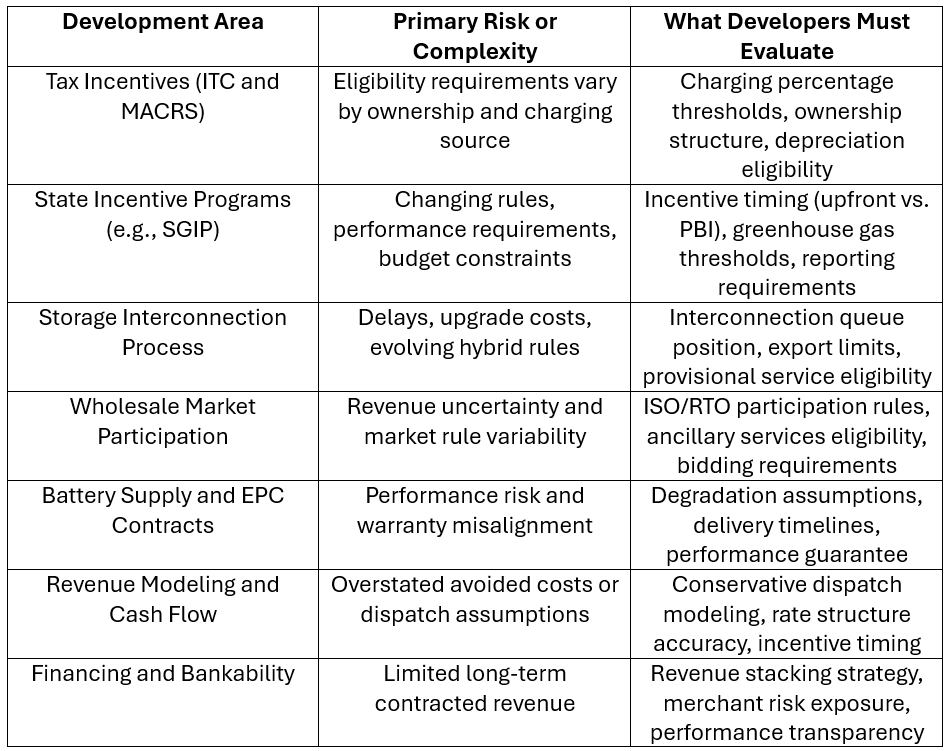

Eligibility depends on system configuration and ownership structure. For commercial projects, storage may qualify for the ITC if the battery is charged by a renewable energy source more than 75% of the time. For residential projects, eligibility has historically required that the battery be charged exclusively by the on-site solar system.

MACRS eligibility varies depending on ownership. Privately owned systems may qualify for accelerated depreciation, while publicly owned projects, such as those owned by government entities or public schools, typically do not.

State-level incentives add another layer of complexity. Programs differ by jurisdiction, funding availability, and performance requirements. Developers must understand how incentives are structured, how and when funds are disbursed, and how they interact with federal tax treatment. Modeling these variables accurately is critical to setting realistic avoided cost assumptions and investor expectations.

Many of these policy interpretations and regulatory considerations are explored in resources such as the Energy Storage Handbook, which outlines how federal and state policies affect storage project development.

SGIP and Incentive Program Complexity

Programs like SGIP can materially improve storage economics, but they introduce compliance and reporting requirements. Recent program updates have included:

- Performance-based incentive structures

- Greenhouse gas reduction thresholds

- Cycling requirements for commercial systems

- Time-of-use rate participation for certain residential customers

- Fleet-level reporting requirements

Incentives may be paid upfront or distributed over time, which directly affects cash flow modeling. Developers must account for incentive timing, performance thresholds, and potential penalties for underperformance. Because program rules evolve, assumptions should be revisited regularly to avoid overstating value.

Accurate modeling platforms that integrate current incentive structures can reduce administrative burden and improve transparency in financial projections.Developers should also stay informed about funding availability and program allocations, including updates to the latest SGIP budget, which can influence project timing and eligibility.

Federal Regulatory Updates and Market Participation

Regulatory reform has played a significant role in expanding storage participation in wholesale markets. FERC Orders 841 and 845 were introduced to better integrate energy storage into wholesale energy, capacity, and ancillary services markets. Among other provisions, market operators must:

- Establish participation models for storage

- Recognize storage’s physical and operational characteristics in bidding

- Allow storage resources to buy and sell energy

- Enable storage to set wholesale market clearing prices, where applicable

These reforms have made it easier to pair storage with renewable generation and clarified interconnection procedures. Provisional interconnection service and greater flexibility around capacity ratings have reduced friction for hybrid projects.

Even so, developers must evaluate how market rules apply in each ISO or RTO territory. Revenue stacking opportunities vary by region, and wholesale participation requires dispatch accuracy and operational transparency.

Key Development Hurdles in the Energy Storage Market

Core Development Hurdles

Despite policy progress, several recurring development challenges remain:

- Evolving business models

- Inconsistent site host agreements

- Fire code and zoning requirements

- EPC and battery supply agreements

- Warranty alignment with expected performance

- Counterparty risk

Battery supply agreements must address delivery timelines, degradation assumptions, and warranty coverage. EPC contracts should align with performance guarantees and interconnection schedules. Developers must also evaluate utility creditworthiness and long-term rate stability, especially when avoided cost savings drive project economics.

Clarity around revenue timing is equally important. Some incentives are paid upfront, while others depend on performance over several years. Without disciplined modeling, mismatches between expected and realized revenue can erode investor confidence.

Financing and Monetizing Storage Projects

Energy storage requires significant capital, and financing structures are still maturing. Investors are generally comfortable with solar because of its long performance history and contracted revenue streams such as power purchase agreements. Storage presents additional uncertainty.

Common financing challenges include:

- Limited long-term contracted revenue

- Technology performance risk

- Operational optimization requirements

- Shorter track record compared to solar

Optimizing storage dispatch often requires active management supported by advanced software. Revenue certainty depends on accurate modeling of rate structures, demand response participation, and wholesale market signals. Many developers rely on advanced energy management software like ETB Controller to support performance modeling and dispatch optimization.

Successful financing typically comes back to fundamentals:

- Transparent revenue assumptions

- Clearly defined dispatch strategy

- Reliable system performance

- Conservative degradation modeling

Financial models may take many forms: shared savings, leases, energy services agreements, or hybrid structures. Regardless of structure, investors expect disciplined analysis and realistic projections.

Moving Forward With Confidence

The energy storage market continues to grow, but growth alone does not eliminate risk. Incentives change, regulations evolve, and project structures vary widely by jurisdiction and customer segment.

Developers who succeed in this environment share several traits: they understand incentive mechanics, model avoided costs conservatively, align technical performance with financial assumptions, prioritize transparency with investors and customers, and rely on precise tools like ETB Developer.

With ETB Developer, you can precisely calculate energy savings, model project economics, seamlessly enroll in demand response programs, and create winning proposals that close deals. Sign up for a 14-day free trial to start modeling and deploying storage with confidence today.

See the full webinar recording here: